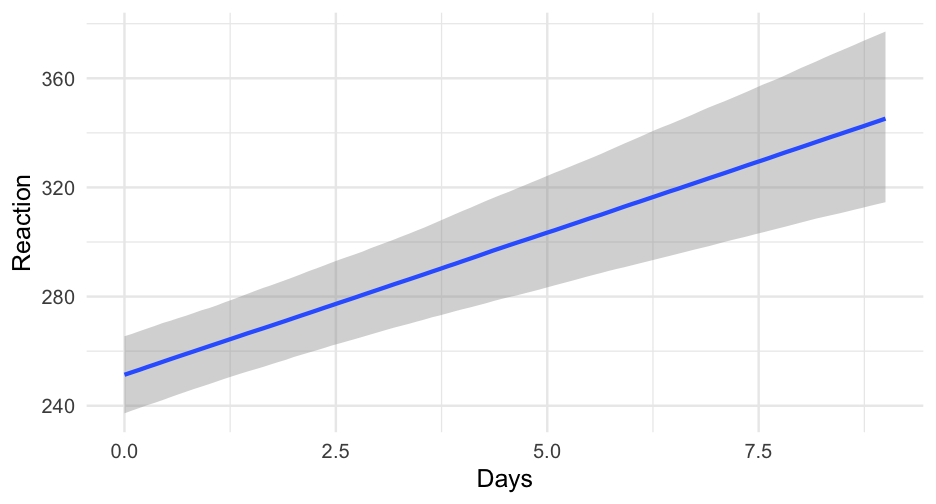

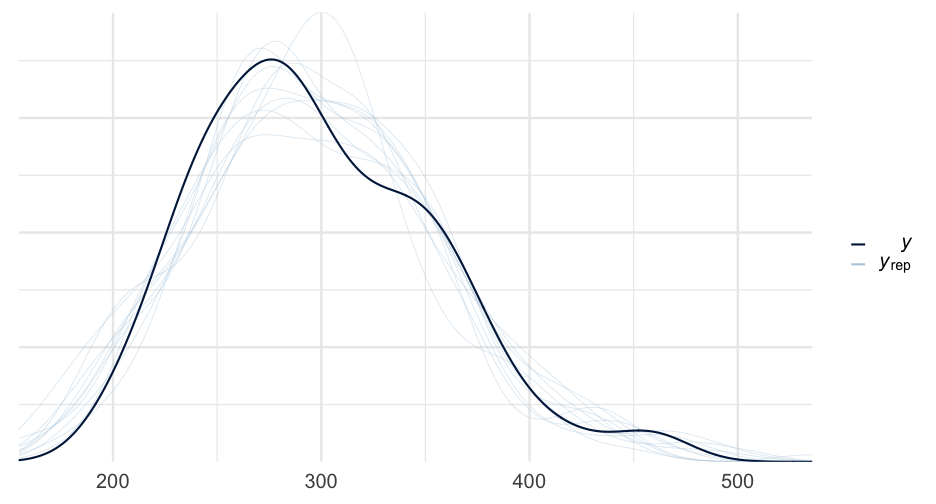

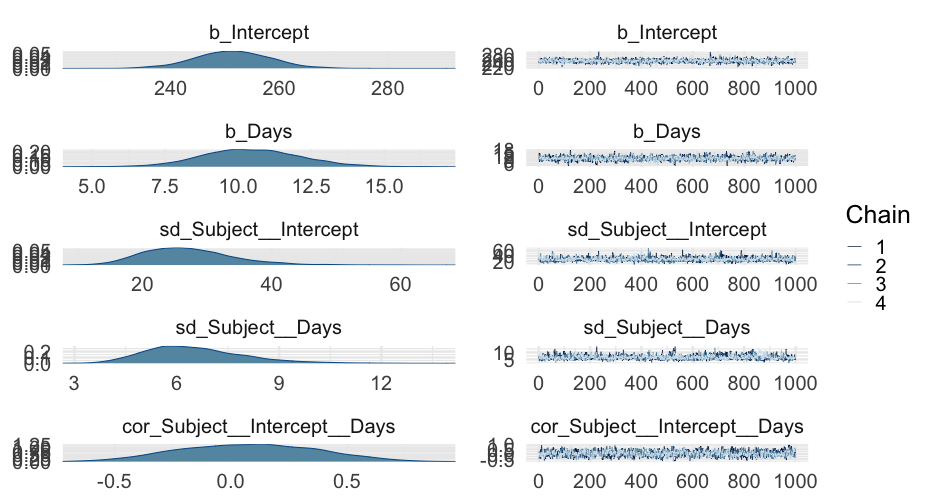

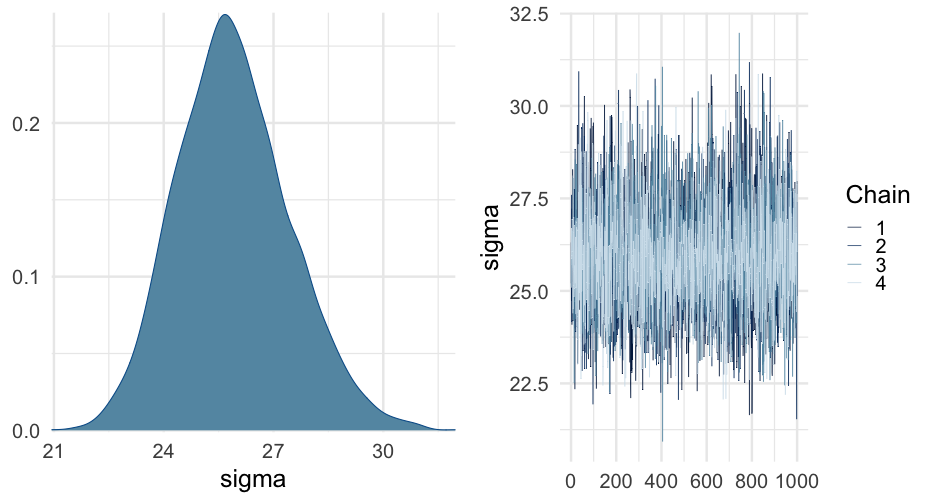

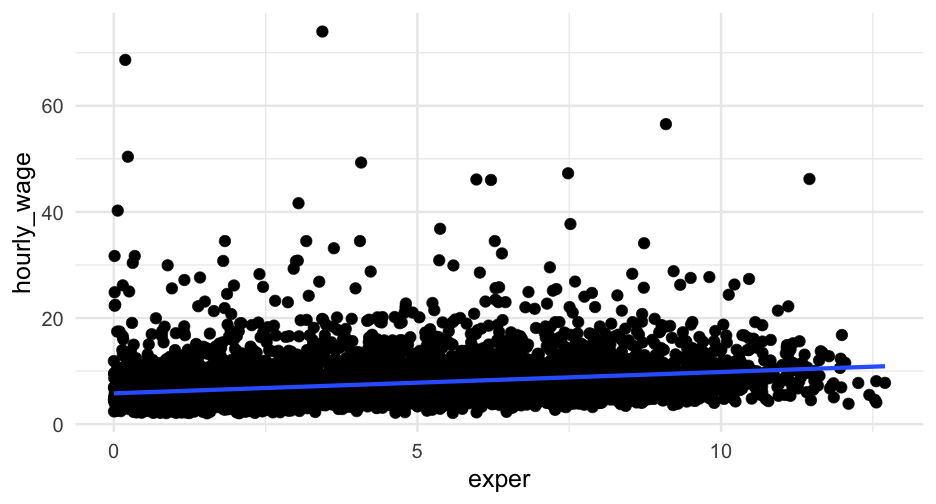

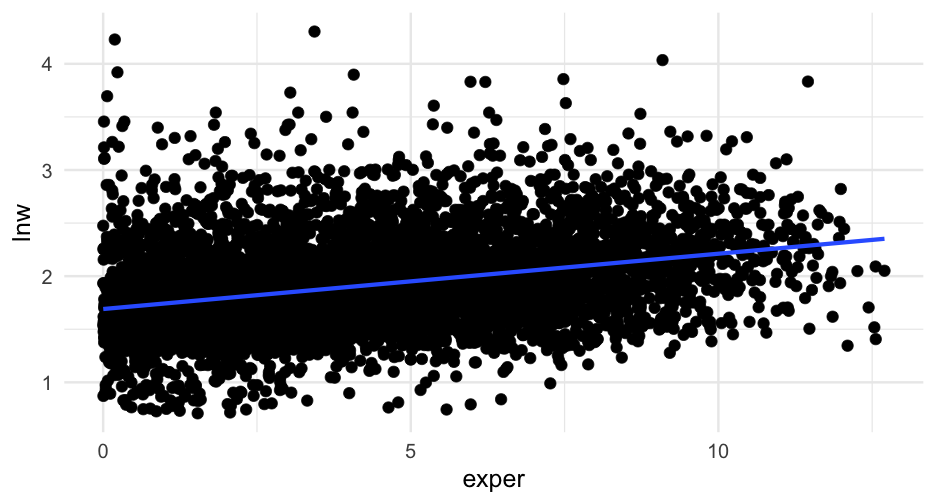

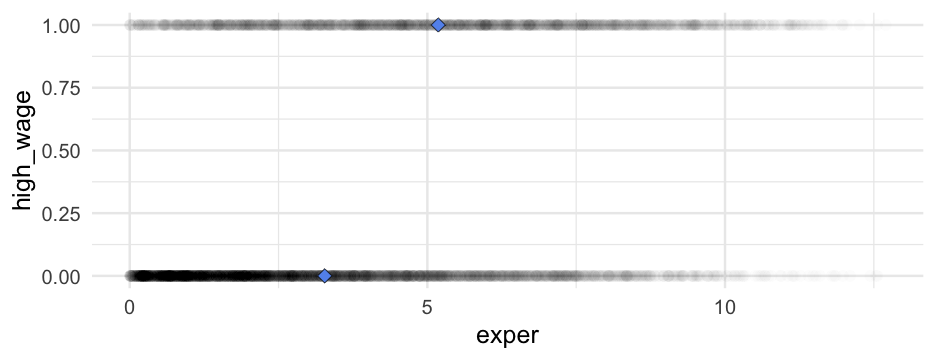

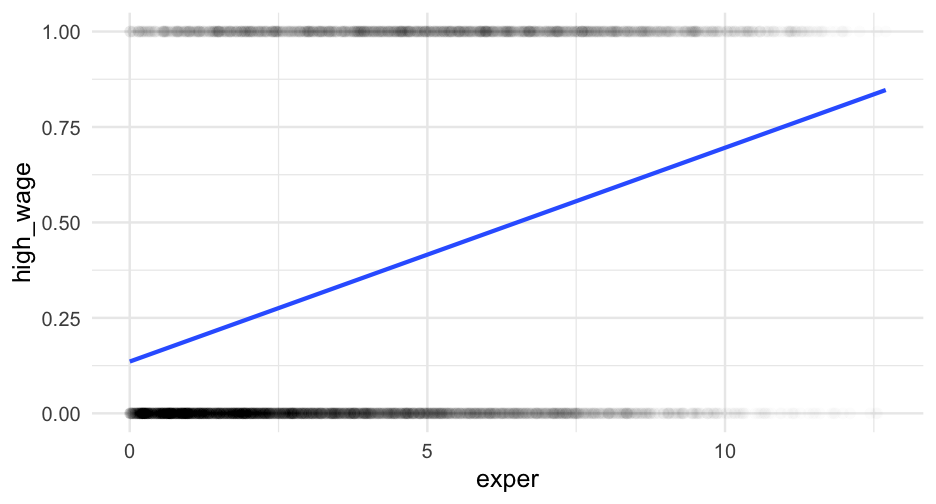

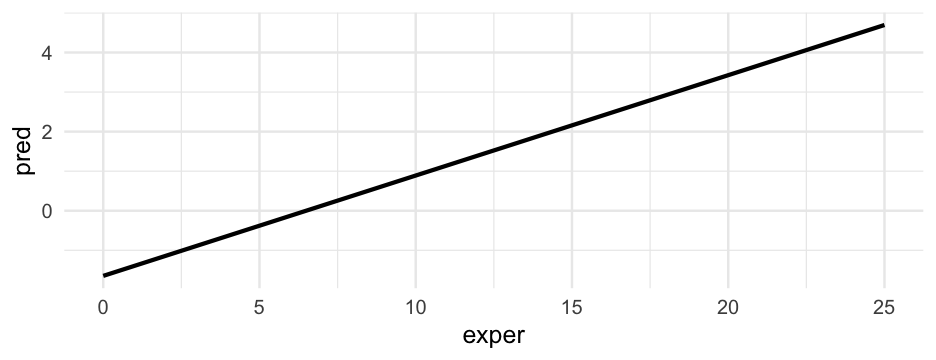

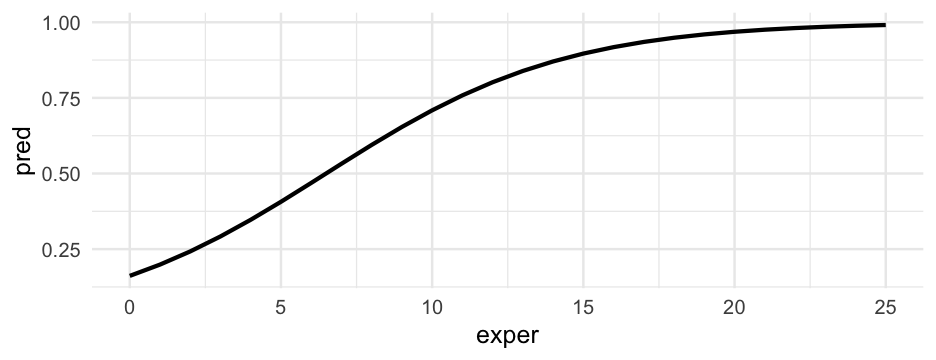

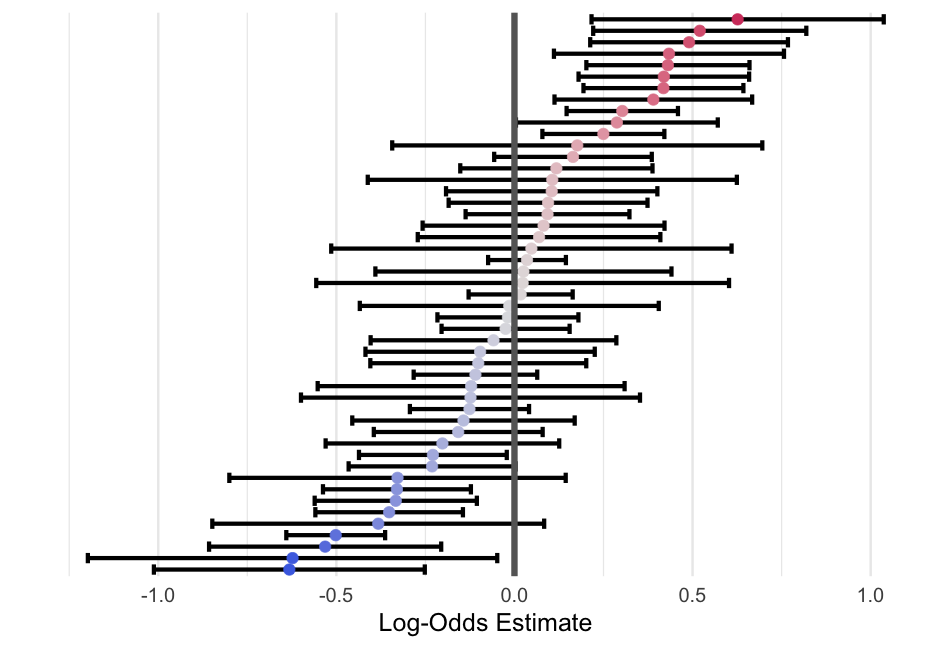

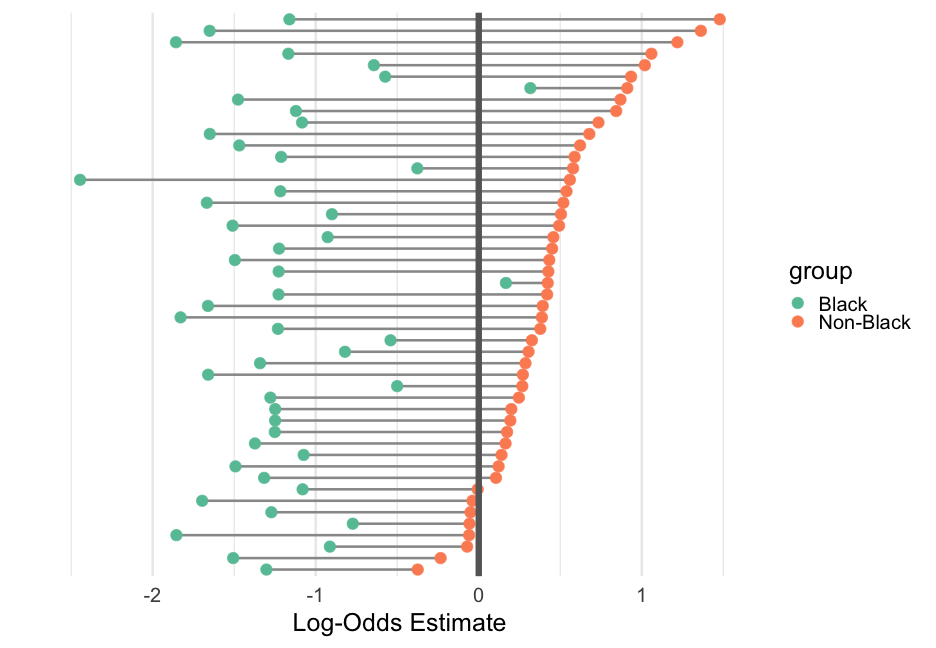

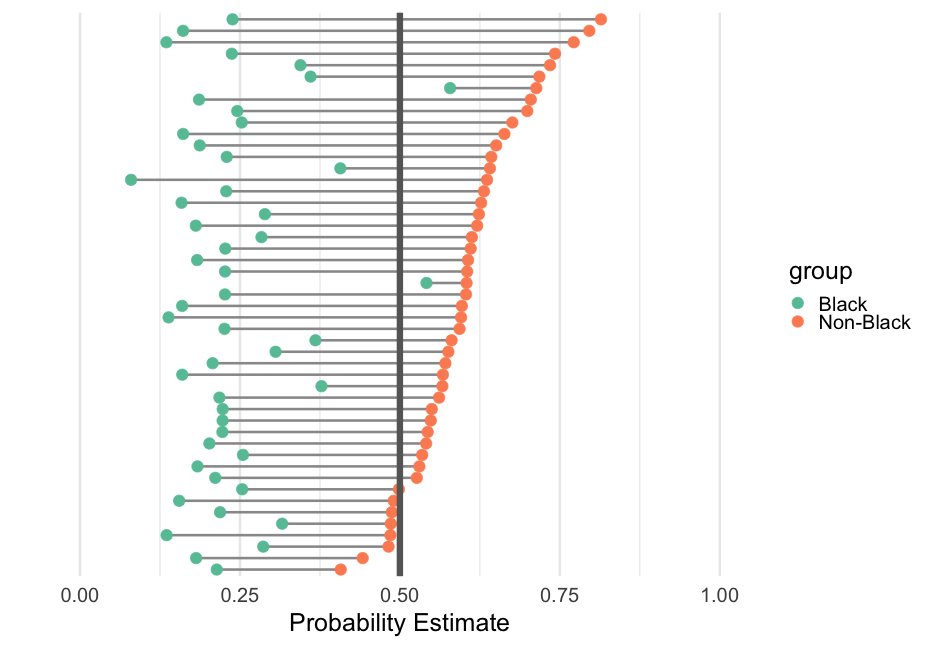

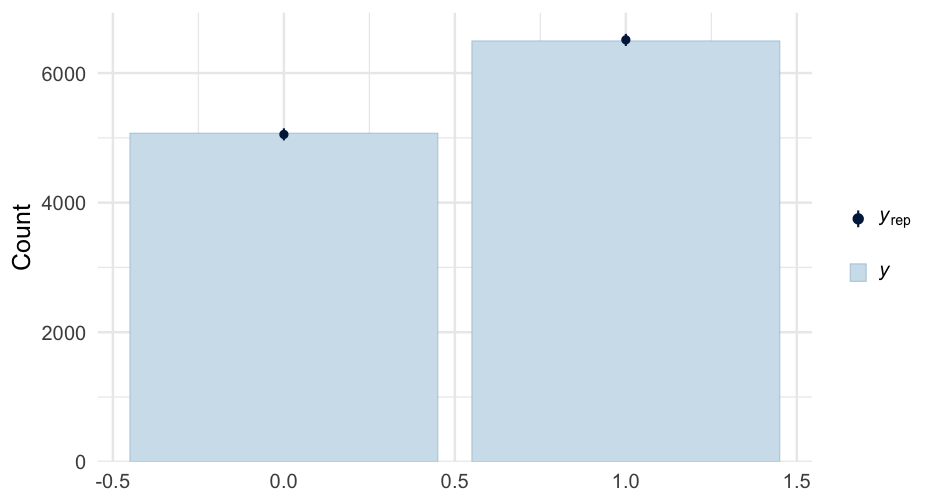

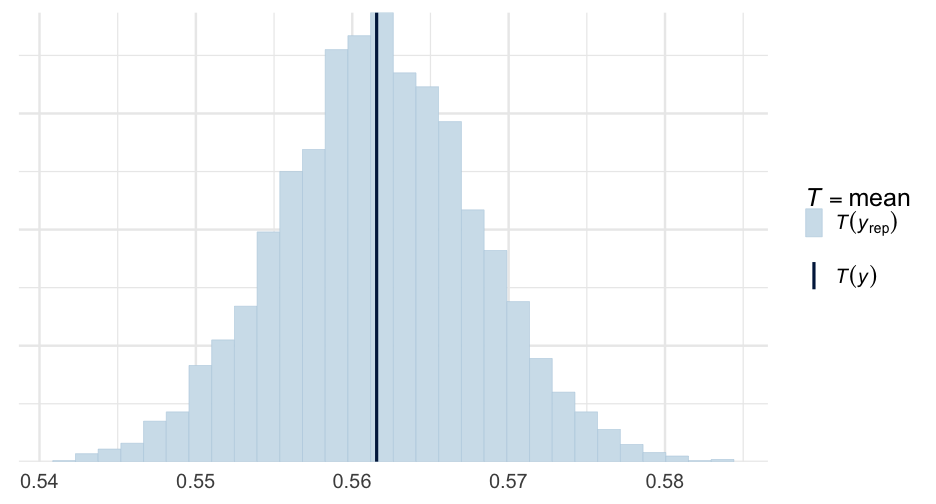

class: center, middle, inverse, title-slide # More Bayes ## And multilevel binomial logistic regression ### Daniel Anderson ### Week 8 --- layout: true <script> feather.replace() </script> <div class="slides-footer"> <span> <a class = "footer-icon-link" href = "https://github.com/datalorax/mlm2/raw/main/static/slides/w8p1.pdf"> <i class = "footer-icon" data-feather="download"></i> </a> <a class = "footer-icon-link" href = "https://mlm2.netlify.app/slides/w8p1.html"> <i class = "footer-icon" data-feather="link"></i> </a> <a class = "footer-icon-link" href = "https://mlm2-2021.netlify.app"> <i class = "footer-icon" data-feather="globe"></i> </a> <a class = "footer-icon-link" href = "https://github.com/datalorax/mlm2"> <i class = "footer-icon" data-feather="github"></i> </a> </span> </div> --- # Agenda * More equation practice * Finishing up our intro to Bayes + Specific focus on MCMC * Implementation with **{brms}** * Logistic regression review * Extending to multilevel logistic regression models with **lme4** --- class: inverse-blue middle # Equation practice --- # The data Read in the following data ```r library(tidyverse) library(lme4) d <- read_csv(here::here("data", "three-lev.csv")) d ``` ``` ## # A tibble: 7,230 x 12 ## schid sid size lowinc mobility female black hispanic retained grade year math ## <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> ## 1 2020 273026452 380 40.3 12.5 0 0 1 0 2 0.5 1.146 ## 2 2020 273026452 380 40.3 12.5 0 0 1 0 3 1.5 1.134 ## 3 2020 273026452 380 40.3 12.5 0 0 1 0 4 2.5 2.3 ## 4 2020 273030991 380 40.3 12.5 0 0 0 0 0 -1.5 -1.303 ## 5 2020 273030991 380 40.3 12.5 0 0 0 0 1 -0.5 0.439 ## 6 2020 273030991 380 40.3 12.5 0 0 0 0 2 0.5 2.43 ## 7 2020 273030991 380 40.3 12.5 0 0 0 0 3 1.5 2.254 ## 8 2020 273030991 380 40.3 12.5 0 0 0 0 4 2.5 3.873 ## 9 2020 273059461 380 40.3 12.5 0 0 1 0 0 -1.5 -1.384 ## 10 2020 273059461 380 40.3 12.5 0 0 1 0 1 -0.5 0.338 ## # … with 7,220 more rows ``` --- # Model 1 Fit the following model <div class="countdown" id="timer_60b908ed" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">30</span></code> </div> $$ `\begin{aligned} \operatorname{math}_{i} &\sim N \left(\alpha_{j[i]}, \sigma^2 \right) \\ \alpha_{j} &\sim N \left(\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{mobility}), \sigma^2_{\alpha_{j}} \right) \text{, for schid j = 1,} \dots \text{,J} \end{aligned}` $$ -- ```r lmer(math ~ mobility + (1|schid), data = d) ``` --- # Model 2 Fit the following model <div class="countdown" id="timer_60b9087a" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">30</span></code> </div> $$ `\begin{aligned} \operatorname{math}_{i} &\sim N \left(\alpha_{j[i],k[i]} + \beta_{1j[i]}(\operatorname{year}), \sigma^2 \right) \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{j} \\ &\beta_{1j} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{female}) \\ &\mu_{\beta_{1j}} \end{aligned} \end{array} \right) , \left( \begin{array}{cc} \sigma^2_{\alpha_{j}} & \rho_{\alpha_{j}\beta_{1j}} \\ \rho_{\beta_{1j}\alpha_{j}} & \sigma^2_{\beta_{1j}} \end{array} \right) \right) \text{, for sid j = 1,} \dots \text{,J} \\ \alpha_{k} &\sim N \left(\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{mobility}), \sigma^2_{\alpha_{k}} \right) \text{, for schid k = 1,} \dots \text{,K} \end{aligned}` $$ -- ```r lmer(math ~ year + female + mobility + (year|sid) + (1|schid), data = d) ``` --- # Model 3 Fit the following model <div class="countdown" id="timer_60b9081d" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">30</span></code> </div> $$ \small `\begin{aligned} \operatorname{math}_{i} &\sim N \left(\alpha_{j[i],k[i]} + \beta_{1j[i]}(\operatorname{year}), \sigma^2 \right) \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{j} \\ &\beta_{1j} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{black}) + \gamma_{2}^{\alpha}(\operatorname{hispanic}) + \gamma_{3}^{\alpha}(\operatorname{female}) \\ &\gamma^{\beta_{1}}_{0} + \gamma^{\beta_{1}}_{1}(\operatorname{black}) + \gamma^{\beta_{1}}_{2}(\operatorname{hispanic}) \end{aligned} \end{array} \right) , \left( \begin{array}{cc} \sigma^2_{\alpha_{j}} & \rho_{\alpha_{j}\beta_{1j}} \\ \rho_{\beta_{1j}\alpha_{j}} & \sigma^2_{\beta_{1j}} \end{array} \right) \right) \text{, for sid j = 1,} \dots \text{,J} \\ \alpha_{k} &\sim N \left(\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{mobility}), \sigma^2_{\alpha_{k}} \right) \text{, for schid k = 1,} \dots \text{,K} \end{aligned}` $$ -- ```r lmer(math ~ year * black + year * hispanic + female + mobility + (year|sid) + (1|schid), data = d) ``` --- # Model 4 Fit the following model <div class="countdown" id="timer_60b90659" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">30</span></code> </div> $$ \small `\begin{aligned} \operatorname{math}_{i} &\sim N \left(\alpha_{j[i],k[i]} + \beta_{1j[i],k[i]}(\operatorname{year}), \sigma^2 \right) \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{j} \\ &\beta_{1j} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1k[i]}^{\alpha}(\operatorname{female}) \\ &\gamma^{\beta_{1}}_{0} + \gamma^{\beta_{1}}_{1}(\operatorname{female}) \end{aligned} \end{array} \right) , \left( \begin{array}{cc} \sigma^2_{\alpha_{j}} & \rho_{\alpha_{j}\beta_{1j}} \\ \rho_{\beta_{1j}\alpha_{j}} & \sigma^2_{\beta_{1j}} \end{array} \right) \right) \text{, for sid j = 1,} \dots \text{,J} \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{k} \\ &\beta_{1k} \\ &\gamma_{1k} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{mobility}) + \gamma_{2}^{\alpha}(\operatorname{lowinc}) \\ &\gamma^{\beta_{1}}_{0} + \gamma^{\beta_{1}}_{1}(\operatorname{mobility}) \\ &\mu_{\gamma_{1k}} \end{aligned} \end{array} \right) , \left( \begin{array}{ccc} \sigma^2_{\alpha_{k}} & \rho_{\alpha_{k}\beta_{1k}} & \rho_{\alpha_{k}\gamma_{1k}} \\ \rho_{\beta_{1k}\alpha_{k}} & \sigma^2_{\beta_{1k}} & \rho_{\beta_{1k}\gamma_{1k}} \\ \rho_{\gamma_{1k}\alpha_{k}} & \rho_{\gamma_{1k}\beta_{1k}} & \sigma^2_{\gamma_{1k}} \end{array} \right) \right) \text{, for schid k = 1,} \dots \text{,K} \end{aligned}` $$ -- ```r lmer(math ~ year * female + year * mobility + lowinc + (year|sid) + (year + female|schid), data = d) ``` --- # Model 5 Fit the following model Don't worry if you run into convergene warnings <div class="countdown" id="timer_60b90953" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">30</span></code> </div> $$ \scriptsize `\begin{aligned} \operatorname{math}_{i} &\sim N \left(\alpha_{j[i],k[i]} + \beta_{1j[i],k[i]}(\operatorname{year}), \sigma^2 \right) \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{j} \\ &\beta_{1j} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1k[i]}^{\alpha}(\operatorname{female}) \\ &\gamma^{\beta_{1}}_{1k[i0} + \gamma^{\beta_{1}}_{1k[i]}(\operatorname{female}) \end{aligned} \end{array} \right) , \left( \begin{array}{cc} \sigma^2_{\alpha_{j}} & \rho_{\alpha_{j}\beta_{1j}} \\ \rho_{\beta_{1j}\alpha_{j}} & \sigma^2_{\beta_{1j}} \end{array} \right) \right) \text{, for sid j = 1,} \dots \text{,J} \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{k} \\ &\beta_{1k} \\ &\gamma_{1k} \\ &\gamma^{\beta_{1}}_{1k} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{mobility}) + \gamma_{2}^{\alpha}(\operatorname{lowinc}) \\ &\mu_{\beta_{1k}} \\ &\mu_{\gamma_{1k}} \\ &\mu_{\gamma^{\beta_{1}}_{1k}} \end{aligned} \end{array} \right) , \left( \begin{array}{cccc} \sigma^2_{\alpha_{k}} & 0 & 0 & 0 \\ 0 & \sigma^2_{\beta_{1k}} & 0 & 0 \\ 0 & 0 & \sigma^2_{\gamma_{1k}} & 0 \\ 0 & 0 & 0 & \sigma^2_{\gamma^{\beta_{1}}_{1k}} \end{array} \right) \right) \text{, for schid k = 1,} \dots \text{,K} \end{aligned}` $$ -- ```r lmer(math ~ year * female + mobility + lowinc + (year|sid) + (year * female||schid), data = d) ``` --- # Model 6 Fit the following model <div class="countdown" id="timer_60b907e4" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">30</span></code> </div> $$ `\begin{aligned} \operatorname{math}_{i} &\sim N \left(\alpha_{j[i]} + \beta_{1j[i]}(\operatorname{year}), \sigma^2 \right) \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{j} \\ &\beta_{1j} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{female}) \\ &\mu_{\beta_{1j}} \end{aligned} \end{array} \right) , \left( \begin{array}{cc} \sigma^2_{\alpha_{j}} & \rho_{\alpha_{j}\beta_{1j}} \\ \rho_{\beta_{1j}\alpha_{j}} & \sigma^2_{\beta_{1j}} \end{array} \right) \right) \text{, for sid j = 1,} \dots \text{,J} \\ \gamma_{1k} &\sim N \left(\mu_{\gamma_{1k}}, \sigma^2_{\gamma_{1k}} \right) \text{, for schid k = 1,} \dots \text{,K} \end{aligned}` $$ -- ```r lmer(math ~ year + female + mobility * size + (year|sid) + (0 + mobility|schid), data = d) ``` --- # Model 7 Fit the following model <div class="countdown" id="timer_60b90722" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">30</span></code> </div> $$ \scriptsize `\begin{aligned} \operatorname{math}_{i} &\sim N \left(\alpha_{j[i]} + \beta_{1j[i]}(\operatorname{year}), \sigma^2 \right) \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{j} \\ &\beta_{1j} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{female}) + \gamma_{2}^{\alpha}(\operatorname{mobility}) + \gamma_{3}^{\alpha}(\operatorname{size}) \\ &\mu_{\beta_{1j}} \end{aligned} \end{array} \right) , \left( \begin{array}{cc} \sigma^2_{\alpha_{j}} & \rho_{\alpha_{j}\beta_{1j}} \\ \rho_{\beta_{1j}\alpha_{j}} & \sigma^2_{\beta_{1j}} \end{array} \right) \right) \text{, for sid j = 1,} \dots \text{,J} \end{aligned}` $$ -- ```r lmer(math ~ year + female + mobility + size + (year|sid), data = d) ``` --- # Model 8 Last one <div class="countdown" id="timer_60b907c6" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">30</span></code> </div> $$ \scriptsize `\begin{aligned} \operatorname{math}_{i} &\sim N \left(\alpha_{j[i],k[i]} + \beta_{1j[i],k[i]}(\operatorname{year}), \sigma^2 \right) \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{j} \\ &\beta_{1j} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{female}) \\ &\mu_{\beta_{1j}} \end{aligned} \end{array} \right) , \left( \begin{array}{cc} \sigma^2_{\alpha_{j}} & \rho_{\alpha_{j}\beta_{1j}} \\ \rho_{\beta_{1j}\alpha_{j}} & \sigma^2_{\beta_{1j}} \end{array} \right) \right) \text{, for sid j = 1,} \dots \text{,J} \\ \left( \begin{array}{c} \begin{aligned} &\alpha_{k} \\ &\beta_{1k} \end{aligned} \end{array} \right) &\sim N \left( \left( \begin{array}{c} \begin{aligned} &\gamma_{0}^{\alpha} + \gamma_{1}^{\alpha}(\operatorname{lowinc}) \\ &\gamma^{\beta_{1}}_{0} + \gamma^{\beta_{1}}_{1}(\operatorname{lowinc}) \end{aligned} \end{array} \right) , \left( \begin{array}{cc} \sigma^2_{\alpha_{k}} & \rho_{\alpha_{k}\beta_{1k}} \\ \rho_{\beta_{1k}\alpha_{k}} & \sigma^2_{\beta_{1k}} \end{array} \right) \right) \text{, for schid k = 1,} \dots \text{,K} \end{aligned}` $$ -- ```r lmer(math ~ year * lowinc + female + (year|sid) + (year |schid), data = d) ``` --- class: inverse-blue middle # Finishing up w/Bayes intro --- # Updated beliefs * Remember our posterior is defined by $$ \text{posterior} = \frac{ \text{likelihood} \times \text{prior}}{\text{average likelihood}} $$ -- When we just had a single parameter to estimate, `\(\mu\)`, this was tractable with grid search. -- With even simple linear regression, however, we have three parameters: `\(\alpha\)`, `\(\beta\)`, and `\(\sigma\)` -- Our Bayesian model then becomes considerably more complicated: $$ P(\alpha, \beta, \sigma \mid x) = \frac{ P(x \mid \alpha, \beta, \sigma) \, P(\alpha, \beta, \sigma)}{\iiint \, P(x \mid \alpha, \beta, \sigma) \, P(\alpha, \beta, \sigma) \,d\alpha \,d\beta \,d\sigma} $$ --- # Estimation Rather than trying to compute the integrals, we draw *samples* from the joint posterior distribution. -- This sounds a bit like magic - how do we do this? -- Multiple different algorithms, but all use some form of Markov-Chain Monte-Carlo sampling --- # Conceptually * Imagine the posterior as a hill * We start with the parameters set to random numbers + Estimate the posterior with this values (our spot on the hill) * Try to "walk" around in a way that we get a complete "picture" of the hill from the samples * Use these samples as your posterior distribution --- # An example .footnote[Example from [Ravenzwaaij et al.](https://link.springer.com/article/10.3758/s13423-016-1015-8)] Let's go back to an example where we're trying to estimate the mean with a know standard deviation. -- $$ N(\mu, 15) $$ -- Start with an initial guess, say 110 --- # MCMC One algorithm: * Generate a *proposal* by taking a sample from your best guess according to some distribution, e.g., `\(\text{proposal} \sim N(110, 10)\)`. Suppose we get a value of 108 -- * Observe the actual data. Let's say we have only one point: 100 -- * Compare the "height" of the proposal distribution to height of the current distribution, relative to observed data: `\(N(100|110, 15)\)`, `\(N(100|108, 15)\)` --- # In code ```r dnorm(110, 100, 15) ``` ``` ## [1] 0.02129653 ``` ```r dnorm(108, 100, 15) ``` ``` ## [1] 0.02307026 ``` --- * If probability of target distribution is higher, accept * If probability is lower, randomly select between the two with probability equal to the "heights" (probability of the two distributions) -- * If proposal is accepted - it's the next sample in the chain * Otherwise, the next sample is a copy of current sample -- ## This completes one iteration Next iteration starts by generating a new proposal distribution -- Stop when you have enough samples to have an adequate "picture" --- # Example in code Let's take 5000 samples ```r set.seed(42) # for reproducibility samples <- c( 110, # initial guess rep(NA, 4999) # space for subsequent samples to fill in ) ``` --- # Loop ```r for(i in 2:5000) { # generate proposal distribution proposal <- rnorm(1, mean = samples[i - 1], sd = 10) # calculate current/proposal distribution likelihoood prob_current <- dnorm(samples[i - 1], 100, 15) prob_proposal <- dnorm(proposal, 100, 15) # compute the probability ratio prob_ratio <- prob_proposal / prob_current # Determine which to select if(prob_ratio > runif(1)) { samples[i] <- proposal # accept } else { samples[i] <- samples[i - 1] # reject } } ``` --- # Plot Iteration history ```r tibble(iteration = 1:5000, value = samples) %>% ggplot(aes(iteration, value)) + geom_line() + geom_hline(yintercept = 100, color = "magenta", size = 3) ``` <!-- --> --- # Plot Density ```r tibble(iteration = 1:5000, value = samples) %>% ggplot(aes(value)) + geom_density(fill = "#00b4f5", alpha = 0.7) + geom_vline(xintercept = 100, color = "magenta", size = 3) ``` <!-- --> --- class: inverse-red middle # Bayes Update Script Last week I promised a script to let you play around with priors. I'll show that now ("bayes-update-plotting.R") There's also a MH script I'll quickly show. ### [demo] --- class: inverse-blue middle # Implementation with {brms} Luckily, we don't have to program the MCMC algorithm ourselves .center[  ] --- # What is it? * **b**ayesian **r**egression **m**odeling with **s**tan * Uses [stan](https://mc-stan.org/) as the model backend - basically writes the model code for you then sends it to stan * Allows model syntax similar to **lme4** * Simple specification of priors - defaults are flat * Provides many methods for post-model fitting inference --- # Fit a basic model Let's start with the default (uninformative) priors, and fit a standard, simple-linear regression model ```r library(brms) sleep_m0 <- brm(Reaction ~ Days, data = lme4::sleepstudy) ``` ``` ## ## SAMPLING FOR MODEL 'a3c55247ada09ee979052a314fc29ad7' NOW (CHAIN 1). ## Chain 1: ## Chain 1: Gradient evaluation took 2.2e-05 seconds ## Chain 1: 1000 transitions using 10 leapfrog steps per transition would take 0.22 seconds. ## Chain 1: Adjust your expectations accordingly! ## Chain 1: ## Chain 1: ## Chain 1: Iteration: 1 / 2000 [ 0%] (Warmup) ## Chain 1: Iteration: 200 / 2000 [ 10%] (Warmup) ## Chain 1: Iteration: 400 / 2000 [ 20%] (Warmup) ## Chain 1: Iteration: 600 / 2000 [ 30%] (Warmup) ## Chain 1: Iteration: 800 / 2000 [ 40%] (Warmup) ## Chain 1: Iteration: 1000 / 2000 [ 50%] (Warmup) ## Chain 1: Iteration: 1001 / 2000 [ 50%] (Sampling) ## Chain 1: Iteration: 1200 / 2000 [ 60%] (Sampling) ## Chain 1: Iteration: 1400 / 2000 [ 70%] (Sampling) ## Chain 1: Iteration: 1600 / 2000 [ 80%] (Sampling) ## Chain 1: Iteration: 1800 / 2000 [ 90%] (Sampling) ## Chain 1: Iteration: 2000 / 2000 [100%] (Sampling) ## Chain 1: ## Chain 1: Elapsed Time: 0.050609 seconds (Warm-up) ## Chain 1: 0.017419 seconds (Sampling) ## Chain 1: 0.068028 seconds (Total) ## Chain 1: ## ## SAMPLING FOR MODEL 'a3c55247ada09ee979052a314fc29ad7' NOW (CHAIN 2). ## Chain 2: ## Chain 2: Gradient evaluation took 6e-06 seconds ## Chain 2: 1000 transitions using 10 leapfrog steps per transition would take 0.06 seconds. ## Chain 2: Adjust your expectations accordingly! ## Chain 2: ## Chain 2: ## Chain 2: Iteration: 1 / 2000 [ 0%] (Warmup) ## Chain 2: Iteration: 200 / 2000 [ 10%] (Warmup) ## Chain 2: Iteration: 400 / 2000 [ 20%] (Warmup) ## Chain 2: Iteration: 600 / 2000 [ 30%] (Warmup) ## Chain 2: Iteration: 800 / 2000 [ 40%] (Warmup) ## Chain 2: Iteration: 1000 / 2000 [ 50%] (Warmup) ## Chain 2: Iteration: 1001 / 2000 [ 50%] (Sampling) ## Chain 2: Iteration: 1200 / 2000 [ 60%] (Sampling) ## Chain 2: Iteration: 1400 / 2000 [ 70%] (Sampling) ## Chain 2: Iteration: 1600 / 2000 [ 80%] (Sampling) ## Chain 2: Iteration: 1800 / 2000 [ 90%] (Sampling) ## Chain 2: Iteration: 2000 / 2000 [100%] (Sampling) ## Chain 2: ## Chain 2: Elapsed Time: 0.048009 seconds (Warm-up) ## Chain 2: 0.021626 seconds (Sampling) ## Chain 2: 0.069635 seconds (Total) ## Chain 2: ## ## SAMPLING FOR MODEL 'a3c55247ada09ee979052a314fc29ad7' NOW (CHAIN 3). ## Chain 3: ## Chain 3: Gradient evaluation took 1.2e-05 seconds ## Chain 3: 1000 transitions using 10 leapfrog steps per transition would take 0.12 seconds. ## Chain 3: Adjust your expectations accordingly! ## Chain 3: ## Chain 3: ## Chain 3: Iteration: 1 / 2000 [ 0%] (Warmup) ## Chain 3: Iteration: 200 / 2000 [ 10%] (Warmup) ## Chain 3: Iteration: 400 / 2000 [ 20%] (Warmup) ## Chain 3: Iteration: 600 / 2000 [ 30%] (Warmup) ## Chain 3: Iteration: 800 / 2000 [ 40%] (Warmup) ## Chain 3: Iteration: 1000 / 2000 [ 50%] (Warmup) ## Chain 3: Iteration: 1001 / 2000 [ 50%] (Sampling) ## Chain 3: Iteration: 1200 / 2000 [ 60%] (Sampling) ## Chain 3: Iteration: 1400 / 2000 [ 70%] (Sampling) ## Chain 3: Iteration: 1600 / 2000 [ 80%] (Sampling) ## Chain 3: Iteration: 1800 / 2000 [ 90%] (Sampling) ## Chain 3: Iteration: 2000 / 2000 [100%] (Sampling) ## Chain 3: ## Chain 3: Elapsed Time: 0.041524 seconds (Warm-up) ## Chain 3: 0.020323 seconds (Sampling) ## Chain 3: 0.061847 seconds (Total) ## Chain 3: ## ## SAMPLING FOR MODEL 'a3c55247ada09ee979052a314fc29ad7' NOW (CHAIN 4). ## Chain 4: ## Chain 4: Gradient evaluation took 7e-06 seconds ## Chain 4: 1000 transitions using 10 leapfrog steps per transition would take 0.07 seconds. ## Chain 4: Adjust your expectations accordingly! ## Chain 4: ## Chain 4: ## Chain 4: Iteration: 1 / 2000 [ 0%] (Warmup) ## Chain 4: Iteration: 200 / 2000 [ 10%] (Warmup) ## Chain 4: Iteration: 400 / 2000 [ 20%] (Warmup) ## Chain 4: Iteration: 600 / 2000 [ 30%] (Warmup) ## Chain 4: Iteration: 800 / 2000 [ 40%] (Warmup) ## Chain 4: Iteration: 1000 / 2000 [ 50%] (Warmup) ## Chain 4: Iteration: 1001 / 2000 [ 50%] (Sampling) ## Chain 4: Iteration: 1200 / 2000 [ 60%] (Sampling) ## Chain 4: Iteration: 1400 / 2000 [ 70%] (Sampling) ## Chain 4: Iteration: 1600 / 2000 [ 80%] (Sampling) ## Chain 4: Iteration: 1800 / 2000 [ 90%] (Sampling) ## Chain 4: Iteration: 2000 / 2000 [100%] (Sampling) ## Chain 4: ## Chain 4: Elapsed Time: 0.048884 seconds (Warm-up) ## Chain 4: 0.020719 seconds (Sampling) ## Chain 4: 0.069603 seconds (Total) ## Chain 4: ``` --- # Model summary ```r summary(sleep_m0) ``` ``` ## Family: gaussian ## Links: mu = identity; sigma = identity ## Formula: Reaction ~ Days ## Data: lme4::sleepstudy (Number of observations: 180) ## Samples: 4 chains, each with iter = 2000; warmup = 1000; thin = 1; ## total post-warmup samples = 4000 ## ## Population-Level Effects: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## Intercept 251.49 6.64 238.26 264.74 1.00 4168 3040 ## Days 10.45 1.25 7.98 12.90 1.00 4155 2967 ## ## Family Specific Parameters: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## sigma 47.96 2.51 43.34 53.22 1.00 4069 2959 ## ## Samples were drawn using sampling(NUTS). For each parameter, Bulk_ESS ## and Tail_ESS are effective sample size measures, and Rhat is the potential ## scale reduction factor on split chains (at convergence, Rhat = 1). ``` --- # View "fixed" effect Let's look at our estimated relation between `Days` and `Reaction` -- ```r conditional_effects(sleep_m0) ``` <!-- --> --- # Wrong model Of course, this is the wrong model, we have a multilevel structure <!-- --> --- # Multilevel model Notice the syntax is essentially equivalent to **lme4** ```r sleep_m1 <- brm(Reaction ~ Days + (Days | Subject), data = lme4::sleepstudy) summary(sleep_m1) ``` ``` ## Family: gaussian ## Links: mu = identity; sigma = identity ## Formula: Reaction ~ Days + (Days | Subject) ## Data: lme4::sleepstudy (Number of observations: 180) ## Samples: 4 chains, each with iter = 2000; warmup = 1000; thin = 1; ## total post-warmup samples = 4000 ## ## Group-Level Effects: ## ~Subject (Number of levels: 18) ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## sd(Intercept) 27.06 7.15 15.59 42.69 1.00 1529 2353 ## sd(Days) 6.55 1.49 4.19 10.04 1.00 1144 1440 ## cor(Intercept,Days) 0.08 0.29 -0.47 0.64 1.01 1125 1844 ## ## Population-Level Effects: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## Intercept 251.42 7.17 237.21 265.47 1.00 2093 2543 ## Days 10.45 1.71 7.23 13.95 1.00 1660 2090 ## ## Family Specific Parameters: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## sigma 25.91 1.54 23.13 29.17 1.00 3581 2712 ## ## Samples were drawn using sampling(NUTS). For each parameter, Bulk_ESS ## and Tail_ESS are effective sample size measures, and Rhat is the potential ## scale reduction factor on split chains (at convergence, Rhat = 1). ``` --- # Fixed effect The uncertainty has increased ```r conditional_effects(sleep_m1) ``` <!-- --> --- # Checking your model ```r pp_check(sleep_m1) ``` <!-- --> --- # More checks ```r plot(sleep_m1) ``` <!-- --><!-- --> --- # Even more ```r launch_shinystan(sleep_m1) ``` --- # Model comparison .footnote[See [here](https://arxiv.org/abs/1507.04544) for probably the best paper on this topic to date (imo)] * Two primary (modern) methods + Leave-one-out Cross-Validation (LOO) + Widely Applicable Information Criterion (WAIC) -- Both provide estimates of the *out-of-sample* predictive accuracy of the model. LOO is similar to K-fold CV, while WAIC is similar to AIC/BIC (but an improved version for Bayes models) -- Both can be computed using **brms**. LOO is approximated (not actually refit each time). --- # LOO: M0 ```r loo(sleep_m0) ``` ``` ## ## Computed from 4000 by 180 log-likelihood matrix ## ## Estimate SE ## elpd_loo -953.3 10.5 ## p_loo 3.2 0.5 ## looic 1906.5 21.0 ## ------ ## Monte Carlo SE of elpd_loo is 0.0. ## ## All Pareto k estimates are good (k < 0.5). ## See help('pareto-k-diagnostic') for details. ``` --- # LOO: M1 ```r loo(sleep_m1) ``` ``` ## Warning: Found 3 observations with a pareto_k > 0.7 in model 'sleep_m1'. It is recommended to set 'moment_match = TRUE' in order to perform moment matching for ## problematic observations. ``` ``` ## ## Computed from 4000 by 180 log-likelihood matrix ## ## Estimate SE ## elpd_loo -861.7 22.7 ## p_loo 34.7 8.8 ## looic 1723.3 45.5 ## ------ ## Monte Carlo SE of elpd_loo is NA. ## ## Pareto k diagnostic values: ## Count Pct. Min. n_eff ## (-Inf, 0.5] (good) 175 97.2% 682 ## (0.5, 0.7] (ok) 2 1.1% 2189 ## (0.7, 1] (bad) 1 0.6% 14 ## (1, Inf) (very bad) 2 1.1% 9 ## See help('pareto-k-diagnostic') for details. ``` --- # Plot ```r plot(loo(sleep_m1), label_points = TRUE) ``` ``` ## Warning: Found 3 observations with a pareto_k > 0.7 in model 'sleep_m1'. It is recommended to set 'moment_match = TRUE' in order to perform moment matching for ## problematic observations. ``` <!-- --> --- # Interpretation Large values here (anything above 0.7) is an indication of model misspecification Smaller values do not guarantee a well-specified model, however --- # LOO Compare .footnote[This is a fairly complicated topic, and we won't spend a lot of time on it. See [here](https://mc-stan.org/loo/articles/loo2-example.html) for a bit more information specifically on the functions] The best fitting model will be on top. Use the standard error within your interpretation ```r loo_compare(loo(sleep_m0), loo(sleep_m1)) ``` ``` ## Warning: Found 3 observations with a pareto_k > 0.7 in model 'sleep_m1'. It is recommended to set 'moment_match = TRUE' in order to perform moment matching for ## problematic observations. ``` ``` ## elpd_diff se_diff ## sleep_m1 0.0 0.0 ## sleep_m0 -91.6 21.4 ``` --- # WAIC Similar to other information criteria. ```r waic(sleep_m0) ``` ``` ## ## Computed from 4000 by 180 log-likelihood matrix ## ## Estimate SE ## elpd_waic -953.3 10.5 ## p_waic 3.2 0.5 ## waic 1906.5 21.0 ``` ```r waic(sleep_m1) ``` ``` ## Warning: ## 14 (7.8%) p_waic estimates greater than 0.4. We recommend trying loo instead. ``` ``` ## ## Computed from 4000 by 180 log-likelihood matrix ## ## Estimate SE ## elpd_waic -860.2 22.3 ## p_waic 33.2 8.4 ## waic 1720.5 44.7 ## ## 14 (7.8%) p_waic estimates greater than 0.4. We recommend trying loo instead. ``` --- # Compare You can use `waic` within `loo_compare()` ```r loo_compare(waic(sleep_m0), waic(sleep_m1)) ``` ``` ## Warning: ## 14 (7.8%) p_waic estimates greater than 0.4. We recommend trying loo instead. ``` ``` ## elpd_diff se_diff ## sleep_m1 0.0 0.0 ## sleep_m0 -93.0 21.0 ``` --- # Another model ```r kidney_m0 <- brm(time ~ age + sex, data = kidney) pp_check(kidney_m0, type = "ecdf_overlay") ``` <!-- --> --- # Fixing this We need to change the assumptions of our model - specifically that the outcome is not normally distributed -- ### Plot the raw data ```r ggplot(kidney, aes(time)) + geom_histogram(alpha = 0.7) ``` <!-- --> --- # Maybe Poisson? (I realize we haven't talked about these types of models yet) ```r kidney_m1 <- brm(time ~ age + sex, data = kidney, family = poisson()) ``` --- # Nope ```r pp_check(kidney_m1, type = "ecdf_overlay") ``` <!-- --> --- # Gamma w/log link ```r kidney_m2 <- brm(time ~ age + sex, data = kidney, family = Gamma("log")) pp_check(kidney_m2, type = "ecdf_overlay") ``` <!-- --> --- # Specifying priors Let's sample from *only* our priors to see what kind of predictions we get. Here, we're specifying that our beta coefficient prior is `\(\beta \sim N(0, 0.5)\)` ```r kidney_m3 <- brm( time ~ age + sex, data = kidney, family = Gamma("log"), prior = prior(normal(0, 0.5), class = "b"), sample_prior = "only" ) ``` --- ```r kidney_m3 ``` ``` ## Warning: There were 2253 divergent transitions after warmup. Increasing adapt_delta above 0.8 may help. See http://mc-stan.org/misc/warnings.html#divergent- ## transitions-after-warmup ``` ``` ## Family: gamma ## Links: mu = log; shape = identity ## Formula: time ~ age + sex ## Data: kidney (Number of observations: 76) ## Samples: 4 chains, each with iter = 2000; warmup = 1000; thin = 1; ## total post-warmup samples = 4000 ## ## Population-Level Effects: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## Intercept 4.23 22.42 -39.94 46.55 1.01 629 991 ## age -0.02 0.51 -0.97 0.97 1.01 629 946 ## sexfemale 0.01 0.50 -0.98 0.97 1.01 667 1196 ## ## Family Specific Parameters: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## shape 0.42 3.64 0.00 2.35 1.01 436 711 ## ## Samples were drawn using sampling(NUTS). For each parameter, Bulk_ESS ## and Tail_ESS are effective sample size measures, and Rhat is the potential ## scale reduction factor on split chains (at convergence, Rhat = 1). ``` --- # Prior predictions Random sample of 100 points <!-- --> --- # Why? It seemed like our prior was fairly tight -- The exploding prior happens because of the log transformation * Age is coded in years * Imagine a coef of 1 (2 standard deviations above our prior) * Prediction for a 25 year old would be `\(\exp(25)\)` = 7.2004899\times 10^{10} --- # A note on prior specifications * It's hard * I don't have a ton of good advice * Be particularly careful when you're using distributions that have anything other than an identity link (e.g., log link, as we are here) --- # One more model Let's fit a model we've fit previously -- In Week 4, we fit this model ```r library(lme4) popular <- read_csv(here::here("data", "popularity.csv")) m_lmer <- lmer(popular ~ extrav + (extrav|class), popular, control = lmerControl(optimizer = "bobyqa")) ``` -- Try fitting the same model with **{brms}** with the default, diffuse priors <div class="countdown" id="timer_60b9088a" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">02</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">00</span></code> </div> --- # Bayesian verision ```r m_brms <- brm(popular ~ extrav + (extrav|class), popular) ``` ``` ## Family: gaussian ## Links: mu = identity; sigma = identity ## Formula: popular ~ extrav + (extrav | class) ## Data: popular (Number of observations: 2000) ## Samples: 4 chains, each with iter = 2000; warmup = 1000; thin = 1; ## total post-warmup samples = 4000 ## ## Group-Level Effects: ## ~class (Number of levels: 100) ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## sd(Intercept) 1.72 0.17 1.41 2.08 1.00 1165 2052 ## sd(extrav) 0.16 0.03 0.11 0.22 1.01 724 1755 ## cor(Intercept,extrav) -0.95 0.03 -1.00 -0.89 1.01 358 564 ## ## Population-Level Effects: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## Intercept 2.46 0.20 2.06 2.84 1.00 994 1951 ## extrav 0.49 0.03 0.44 0.54 1.00 1510 2474 ## ## Family Specific Parameters: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## sigma 0.95 0.02 0.92 0.98 1.00 4787 2392 ## ## Samples were drawn using sampling(NUTS). For each parameter, Bulk_ESS ## and Tail_ESS are effective sample size measures, and Rhat is the potential ## scale reduction factor on split chains (at convergence, Rhat = 1). ``` --- # lme4 model ```r arm::display(m_lmer) ``` ``` ## lmer(formula = popular ~ extrav + (extrav | class), data = popular, ## control = lmerControl(optimizer = "bobyqa")) ## coef.est coef.se ## (Intercept) 2.46 0.20 ## extrav 0.49 0.03 ## ## Error terms: ## Groups Name Std.Dev. Corr ## class (Intercept) 1.73 ## extrav 0.16 -0.97 ## Residual 0.95 ## --- ## number of obs: 2000, groups: class, 100 ## AIC = 5791.4, DIC = 5762 ## deviance = 5770.7 ``` --- # Add priors * Multiple ways to do this * Generally, I allow the intercept to just be what it is * For "fixed" effects, you might consider [regularizing](https://vasishth.github.io/bayescogsci/book/sec-sensitivity.html#regularizing-priors) priors. * You can also set priors for individual parameters * In my experience, you will mostly want to set priors for different "class"es of parameters, e.g.: `Intercept`, `b`, `sd`, `sigma`, `cor` --- # Half-Cauchy distribution This is the distribution most often used for standard deviation priors <!-- --> --- # Specify some new priors Let's specify some regularizing priors for the fixed effects and standard deviations -- ```r priors <- c( prior(normal(0, 0.5), class = b), prior(cauchy(0, 1), class = sd) ) m_brms2 <- brm(popular ~ extrav + (extrav|class), data = popular, prior = priors) ``` --- Almost no difference in this case ```r m_brms2 ``` ``` ## Family: gaussian ## Links: mu = identity; sigma = identity ## Formula: popular ~ extrav + (extrav | class) ## Data: popular (Number of observations: 2000) ## Samples: 4 chains, each with iter = 2000; warmup = 1000; thin = 1; ## total post-warmup samples = 4000 ## ## Group-Level Effects: ## ~class (Number of levels: 100) ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## sd(Intercept) 1.70 0.17 1.39 2.06 1.01 1358 1824 ## sd(extrav) 0.16 0.03 0.11 0.22 1.00 871 1683 ## cor(Intercept,extrav) -0.95 0.03 -1.00 -0.88 1.01 437 871 ## ## Population-Level Effects: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## Intercept 2.48 0.20 2.08 2.86 1.00 1157 1810 ## extrav 0.49 0.03 0.44 0.54 1.00 1960 2642 ## ## Family Specific Parameters: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## sigma 0.95 0.02 0.92 0.98 1.00 3976 2977 ## ## Samples were drawn using sampling(NUTS). For each parameter, Bulk_ESS ## and Tail_ESS are effective sample size measures, and Rhat is the potential ## scale reduction factor on split chains (at convergence, Rhat = 1). ``` --- # Speed We'll never reach the `lme4::lmer()` speeds, but we can make it faster. * Parallelize (not always as effective as you might hope) * Use the cmdstan backend + This requires a little bit of additional work, but is probably worth it if you're fitting bigger models. --- # Installing cmdstan First, install the [**{cmdstanr}**](https://mc-stan.org/cmdstanr/articles/cmdstanr.html) package ```r install.packages( "cmdstanr", repos = c( "https://mc-stan.org/r-packages/", getOption("repos") ) ) ``` -- Then, install **cmdstan** ```r cmdstanr::install_cmdstan() ``` --- # Timings I'm not evaluating the below, but the timings were 112.646, 84.561, and 42.934 seconds, respectively. ```r library(tictoc) tic() m_brms <- brm(popular ~ extrav + (extrav|class), data = popular) toc() # cmdstan tic() m_brms2 <- brm(popular ~ extrav + (extrav|class), data = popular, * backend = "cmdstanr") toc() # cmdstan w/parallelization tic() m_brms3 <- brm(popular ~ extrav + (extrav|class), data = popular, backend = "cmdstanr", * cores = 4) toc() ``` --- class: inverse-red middle # Wrapping up our Bayes intro --- # Advantages to Bayes * Opportunity to incorporate prior knowledge into the modeling process (you don't really *have* to - could just set wide priors) * Natural interpretation of uncertainty * Can often allow you to estimate models that are difficult if not impossible with frequentist methods -- ## Disadvatages * Generally going to be slower in implementation * You may run into pushback from others - particularly with respect to priors --- # Notes on the posterior * The posterior is the distribution of the parameters, given the data * Think of it as the distribution of what we don't know, but are interested in (model parameters), given what we know or have observed (the data), and our prior beliefs * Gives a complete picture of parameter uncertainty * We can do lots of things with the posterior that is hard to get otherwise --- class: inverse-green middle # Break .center[ <div class="countdown" id="timer_60b90ab2" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">05</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">00</span></code> </div> ] --- class: inverse-red middle # Review of logistic regression --- # Data generating distribution Up to this point, we've been assuming the data were generated from a normal distribution. -- For example, we might fit a simple linear regression model to the wages data like this $$ `\begin{aligned} \operatorname{wages}_{i} &\sim N \left(\widehat{y}, \sigma^2 \right) \\ \widehat{y} &= \alpha + \beta_{1}(\operatorname{exper}) \end{aligned}` $$ where we're embedding a linear model into the mean -- In code ```r wages <- read_csv(here::here("data", "wages.csv")) %>% mutate(hourly_wage = exp(lnw)) wages_lm <- lm(hourly_wage ~ exper, data = wages) ``` --- # Graphically ```r ggplot(wages, aes(exper, hourly_wage)) + geom_point() + geom_smooth(method = "lm", se = FALSE) ``` <!-- --> -- Aside - you see why the log of wages was modeled instead? --- # Log wages ```r ggplot(wages, aes(exper, lnw)) + geom_point() + geom_smooth(method = "lm", se = FALSE) ``` <!-- --> --- # Move to binary model Let's split the wages data into a binary classification based on whether it's above or below the mean. -- ```r wages <- wages %>% mutate( high_wage = ifelse( hourly_wage > mean(hourly_wage, na.rm = TRUE), 1, 0 ) ) wages %>% select(id, hourly_wage, high_wage) ``` ``` ## # A tibble: 6,402 x 3 ## id hourly_wage high_wage ## <dbl> <dbl> <dbl> ## 1 31 4.441535 0 ## 2 31 4.191254 0 ## 3 31 4.344888 0 ## 4 31 5.748851 0 ## 5 31 6.896403 0 ## 6 31 5.523435 0 ## 7 31 8.052640 1 ## 8 31 8.406456 1 ## 9 36 7.257243 0 ## 10 36 6.037560 0 ## # … with 6,392 more rows ``` --- # Plot ```r means <- wages %>% group_by(high_wage) %>% summarize(mean = mean(exper)) ggplot(wages, aes(exper, high_wage)) + geom_point(alpha = 0.01) + geom_point(aes(x = mean), data = means, shape = 23, fill = "cornflowerblue") ``` <!-- --> --- # We could fit a linear model ```r m_lpm <- lm(high_wage ~ exper, data = wages) arm::display(m_lpm) ``` ``` ## lm(formula = high_wage ~ exper, data = wages) ## coef.est coef.se ## (Intercept) 0.14 0.01 ## exper 0.06 0.00 ## --- ## n = 6402, k = 2 ## residual sd = 0.45, R-Squared = 0.11 ``` -- This is referred to as a linear probability model (LPM) and they are pretty hotly contested, with proponents and detractors --- # Plot ```r ggplot(wages, aes(exper, high_wage)) + geom_point(alpha = 0.01) + geom_smooth(method = "lm", se = FALSE) ``` <!-- --> --- # Prediction What if somebody has an experience of 25 years? -- ```r predict(m_lpm, newdata = data.frame(exper = 25)) ``` ``` ## 1 ## 1.535723 ``` 🤨 Our prediction goes outside the range of our data. -- As a rule, the assumed data generating process should match the boundaries of the data. -- Of course, you could truncate after the fact. I think that's less than ideal (see [here](https://www.alexpghayes.com/blog/consistency-and-the-linear-probability-model/) or [here](https://github.com/alexpghayes/linear-probability-model/blob/master/presentation.pdf) for discussions contrasting LPM with logistic regression). --- # The binomial model $$ y_i \sim \text{Binomial}(n, p_i) $$ -- Think in terms of coin flips -- `\(n\)` is the number of coin flips, while `\(p_i\)` is the probability of heads --- # Example Flip 1 coin 10 times ```r set.seed(42) rbinom( n = 10, # number of trials size = 1, # number of coins prob = 0.5 # probability of heads ) ``` ``` ## [1] 1 1 0 1 1 1 1 0 1 1 ``` -- Side note - a binomial model with `size = 1` (or `\(n = 1\)` in equation form) is equivalent to a Bernoulli distribution -- Flip 10 coins 1 time ```r rbinom(n = 1, size = 10, prob = 0.5) ``` ``` ## [1] 5 ``` --- # Modeling We now build a linear model for `\(p\)`, just like we previously built a linear model for `\(\mu\)`. -- .center[ .realbig[ A problem ] ] Probability is bounded `\([0, 1]\)` We need to ensure that our model respects these bounds --- # Link functions We solve this problem by using a *link* function $$ `\begin{aligned} y_i &\sim \text{Binomial}(n, p_i) \\ f(p_i) &= \alpha + \beta(x_i) \end{aligned}` $$ -- * Instead of modeling `\(p_i\)` directly, we model `\(f(p_i)\)` -- * The specific `\(f\)` is the link function -- * Link functions map the *linear* space of the model to the *non-linear* parameters (like probability) -- * The *log* and *logit* links are most common --- # Binomial logistic regression If we only have two categories, we commonly assume a binomial distribution, with a logit link. $$ `\begin{aligned} y_i &\sim \text{Binomial}(n, p_i) \\ \text{logit}(p_i) &= \alpha + \beta(x_i) \end{aligned}` $$ -- where the logit link is defined by the *log-odds* $$ \text{logit}(p_i) = \log\left[\frac{p_i}{1-p_i}\right] $$ -- So $$ \log\left[\frac{p_i}{1-p_i}\right] = \alpha + \beta(x_i) $$ --- # Inverse link What we probably want to interpret is probability -- We can transform the log-odds to probability by exponentiating $$ p_i = \frac{\exp(\alpha + \beta(x_i))}{1 + \exp(\alpha + \beta(x_i))} $$ -- This is the logistic function, or the inverse-logit. --- # Example logistic regression model ```r m_glm <- glm(high_wage ~ exper, data = wages, * family = binomial(link = "logit")) arm::display(m_glm) ``` ``` ## glm(formula = high_wage ~ exper, family = binomial(link = "logit"), ## data = wages) ## coef.est coef.se ## (Intercept) -1.65 0.05 ## exper 0.25 0.01 ## --- ## n = 6402, k = 2 ## residual deviance = 7655.2, null deviance = 8345.8 (difference = 690.5) ``` --- # Coefficient interpretation The coefficients are reported on the *log-odds* scale. Other than that, interpretation is the same. -- For example: The log-odds of a participant with zero years experience being in the high wage category was -1.65. For every one year of additional experience, the log-odds of being in the high wage category increased by 0.25. --- # Note * Outside of scientific audiences, almost nobody is going to understand the previous slide * You *cannot* just transform the coefficients and interpret them as probabilities (because it is non-linear on the probability scale). --- # Log odds scale ```r tibble(exper = 0:25) %>% mutate(pred = predict(m_glm, newdata = .)) %>% ggplot(aes(exper, pred)) + geom_line() ``` <!-- --> -- Perfectly straight line - change in log-odds are modeled as a linear function of experience --- # Probability scale ```r tibble(exper = 0:25) %>% mutate(pred = predict(m_glm, newdata = ., type = "response")) %>% ggplot(aes(exper, pred)) + geom_line() ``` <!-- --> -- Our model parameters map to probability non-linearly, and it is bound to `\([0, 1]\)` --- # Probability predictions Let's make the predictions from the previous slide "by hand" -- Recall: $$ p_i = \frac{\exp(\alpha + \beta(x_i))}{1 + \exp(\alpha + \beta(x_i))} $$ -- And our coefficients are ```r coef(m_glm) ``` ``` ## (Intercept) exper ## -1.6467568 0.2536815 ``` --- # Intercept $$ (p_i|\text{exper = 0}) = \frac{\exp(-1.65 + 0.25(0))}{1 + \exp(-1.65 + 0.25(0))} $$ -- $$ (p_i|\text{exper = 0}) = \frac{\exp(-1.65)}{1 + \exp(-1.65)} $$ -- $$ (p_i|\text{exper = 0}) = \frac{0.19}{1.19} = 0.16 $$ --- # Five years experience Notice the exponentiation happens *after* adding the coefficients together $$ (p_i|\text{exper = 5}) = \frac{\exp(-1.65 + 0.25(5))}{1 + \exp(-1.65 + 0.25(5))} $$ -- $$ (p_i|\text{exper = 5}) = \frac{\exp(-0.4)}{1 + \exp(-0.4)} $$ -- $$ (p_i|\text{exper = 5}) = \frac{0.67}{1.67} = 0.40 $$ --- # Fifteen years experience $$ (p_i|\text{exper = 15}) = \frac{\exp(-1.65 + 0.25(15))}{1 + \exp(-1.65 + 0.25(15))} $$ -- $$ (p_i|\text{exper = 15}) = \frac{\exp(2.1)}{1 + \exp(2.1)} $$ -- $$ (p_i|\text{exper = 15}) = \frac{8.16}{9.16} = 0.89 $$ --- # More interpretation Let's try to make this so more people might understand. -- First, show the logistic curve on the probability scale! Can help prevent linear interpretations -- Discuss probabilities at different `\(x\)` values -- The "divide by 4" rule --- # Divide by 4 * Logistic curve is steepest when `\(p_i = 0.5\)` * The slope of the logistic curve (its derivative) is maximized at `\(\beta/4\)` * Aside from the intercept, we can say that the change is *no more* than `\(\beta/4\)` -- ## Example $$ \frac{0.25}{4} = 0.0625 $$ -- So, a one year increase in experience corresponds to, at most, a 6% increase in being in the high wage category --- # Example writeup There was a 16 percent chance that a participant with zero years experience would be in the *high wage* category. The logistic function, which mapped years of experience to the probability of being in the *high-wage* category, was non-linear, as shown in Figure 1. At its steepest point, a one year increase in experience corresponded with approximately a 6% increase in the probability of being in the high-wage category. For individuals with 5, 10, and 15 years of experience, the probability increased to a 41, 71, and 90 percent chance, respectively. --- class: inverse-red middle # Other distributions --- background-image: url(img/distributions.png) background-size: contain .footnote[Figure from [McElreath](https://xcelab.net/rm/statistical-rethinking/)] --- class: inverse-blue middle # Multilevel logistic regression --- # The data Polling data from the 1988 election. ```r polls <- rio::import(here::here("data", "polls.dta"), setclass = "tbl_df") polls ``` ``` ## # A tibble: 13,544 x 10 ## org year survey bush state edu age female black weight ## <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> ## 1 1 1 1 1 7 2 2 1 0 1403 ## 2 1 1 1 1 33 4 3 0 0 778 ## 3 1 1 1 0 20 2 1 1 0 1564 ## 4 1 1 1 1 31 3 2 1 0 1055 ## 5 1 1 1 1 18 3 1 1 0 1213 ## 6 1 1 1 1 31 4 2 0 0 910 ## 7 1 1 1 1 40 1 3 0 0 735 ## 8 1 1 1 1 33 4 2 1 0 410 ## 9 1 1 1 0 22 4 2 1 0 410 ## 10 1 1 1 1 22 4 3 0 0 778 ## # … with 13,534 more rows ``` --- # About the data * Collected one week before the election * Nationally representative sample * Should use post-stratification to control for non-response, but we'll hold off on that for now (See Gelman & Hill, Chapter 14 for more details) --- # Baseline probability Let's assume we want to estimate the probability that Bush will be elected. -- We could fit a single level model like this $$ `\begin{aligned} \operatorname{bush} &\sim \text{Binomial}\left(n = 1, \operatorname{prob}_{\operatorname{bush} = \operatorname{1}}= \hat{P}\right) \\ \log\left[ \frac { \hat{P} }{ 1 - \hat{P} } \right] &= \alpha \end{aligned}` $$ --- # In code Can you write the code for the previous model? <div class="countdown" id="timer_60b907e6" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">00</span></code> </div> -- ```r bush_sl <- glm(bush ~ 1, data = polls, family = binomial(link = "logit")) ``` -- ```r arm::display(bush_sl) ``` ``` ## glm(formula = bush ~ 1, family = binomial(link = "logit"), data = polls) ## coef.est coef.se ## (Intercept) 0.25 0.02 ## --- ## n = 11566, k = 1 ## residual deviance = 15858.1, null deviance = 15858.1 (difference = 0.0) ``` -- So, `\(p_i = \frac{\exp(0.25)}{1 + \exp(0.25)} = 0.56\)` --- # State-level variability To estimate state-level variability, we just specify a distribution for the intercept variability. -- $$ `\begin{aligned} \operatorname{bush} &\sim \text{Binomial}\left(n = 1, \operatorname{prob}_{\operatorname{bush} = \operatorname{1}}= \hat{P}\right) \\ \log\left[ \frac { \hat{P} }{ 1 - \hat{P} } \right] &= \alpha_{j[i]} \\ \alpha_{j} &\sim N \left(\mu_{\alpha_{j}}, \sigma^2_{\alpha_{j}} \right) \text{, for state j = 1,} \dots \text{,J} \end{aligned}` $$ -- Notice we're still specifying that the intercept variability is generated by a *normal* distribution. -- What does this variability actually represent? -- Variance in the log-odds --- # Fitting the model If we're using **{lme4}**, we just swap `lmer()` for `glmer()` and specify the family and link function. -- ```r library(lme4) m0 <- glmer(bush ~ 1 + (1|state), data = polls, family = binomial(link = "logit")) arm::display(m0) ``` ``` ## glmer(formula = bush ~ 1 + (1 | state), data = polls, family = binomial(link = "logit")) ## coef.est coef.se ## 0.25 0.06 ## ## Error terms: ## Groups Name Std.Dev. ## state (Intercept) 0.34 ## Residual 1.00 ## --- ## number of obs: 11566, groups: state, 49 ## AIC = 15697, DIC = 15450.4 ## deviance = 15571.7 ``` --- # Interpretation * The average log odds of supporting bush was 0.25 * This average varied between states with a standard deviation of 0.34 --- # State-level variation ```r library(broom.mixed) m0_tidied <- tidy(m0, effects = "ran_vals", conf.int = TRUE) m0_tidied ``` ``` ## # A tibble: 49 x 8 ## effect group level term estimate std.error conf.low conf.high ## <chr> <chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl> ## 1 ran_vals state 1 (Intercept) 0.5201836 0.1526301 0.2210341 0.8193332 ## 2 ran_vals state 3 (Intercept) 0.09438107 0.1424292 -0.1847750 0.3735371 ## 3 ran_vals state 4 (Intercept) 0.06905650 0.1737493 -0.2714859 0.4095989 ## 4 ran_vals state 5 (Intercept) 0.03522421 0.05570977 -0.07396493 0.1444133 ## 5 ran_vals state 6 (Intercept) 0.1045418 0.1513626 -0.1921233 0.4012070 ## 6 ran_vals state 7 (Intercept) -0.1015410 0.1546380 -0.4046260 0.2015440 ## 7 ran_vals state 8 (Intercept) -0.3824312 0.2376744 -0.8482644 0.08340195 ## 8 ran_vals state 9 (Intercept) -0.6229779 0.2931982 -1.197636 -0.04832002 ## 9 ran_vals state 10 (Intercept) 0.3027001 0.07975137 0.1463903 0.4590099 ## 10 ran_vals state 11 (Intercept) 0.09282107 0.1173420 -0.1371651 0.3228072 ## # … with 39 more rows ``` --- # Fancified Plot Code ```r m0_tidied %>% mutate(level = forcats::fct_reorder(level, estimate)) %>% ggplot(aes(estimate, level)) + geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) + geom_point(aes(color = estimate)) + geom_vline(xintercept = 0, color = "gray40", size = 3) + labs(x = "Log-Odds Estimate", y = "") + colorspace::scale_color_continuous_diverging(palette = "Blue-Red 2") + guides(color = "none") + theme(panel.grid.major.y = element_blank(), axis.text.y = element_blank()) ``` --- # Fancified Plot <!-- --> --- # Extending the model Let's add some predictors * Include `age`, `female` and `black` as fixed effect predictors. -- * We should center age so the intercept represents the sample average age. -- You try first <div class="countdown" id="timer_60b90ac0" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">03</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">00</span></code> </div> --- ```r polls <- polls %>% mutate(age_c = age - mean(age, na.rm = TRUE)) m1 <- glmer(bush ~ age_c + female + black + (1|state), data = polls, family = binomial(link = "logit")) arm::display(m1) ``` ``` ## glmer(formula = bush ~ age_c + female + black + (1 | state), ## data = polls, family = binomial(link = "logit")) ## coef.est coef.se ## (Intercept) 0.43 0.07 ## age_c -0.08 0.02 ## female -0.11 0.04 ## black -1.84 0.09 ## ## Error terms: ## Groups Name Std.Dev. ## state (Intercept) 0.41 ## Residual 1.00 ## --- ## number of obs: 11566, groups: state, 49 ## AIC = 15137.1, DIC = 14856.7 ## deviance = 14991.9 ``` --- # Varying slopes The average probability of a respondent who was coded `black == 1` who was the average age and non-female supporting Bush was $$ \small `\begin{equation} (p_i|\text{age} = 0, \text{female} = 0, \text{black} = 1) = \frac{\exp(0.43 + (-0.08 \times 0) + (-0.11 \times 0) + (-1.84 \times 1))}{1 + \exp(0.43 + (-0.08 \times 0) + (-0.11 \times 0) + (-1.84 \times 1))} \end{equation}` $$ -- $$ (p_i|\text{age} = 0, \text{female} = 0, \text{black} = 1) = \frac{\exp(0.43 -1.84))}{1 + \exp(0.43 -1.84)} $$ -- $$ (p_i|\text{age} = 0, \text{female} = 0, \text{black} = 1) = \frac{\exp(-1.41))}{1 + \exp(-1.41)} $$ -- $$ (p_i|\text{age} = 0, \text{female} = 0, \text{black} = 1) = \frac{0.24}{1.24} $$ -- $$ (p_i|\text{age} = 0, \text{female} = 0, \text{black} = 1) = 0.19 $$ --- # Vary by state? You try first - try to fit a model that estimates between-state variability in the relation between individuals coded `black`, and their probability of voting for Bush. <div class="countdown" id="timer_60b909e3" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">01</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">00</span></code> </div> -- ```r m2 <- glmer(bush ~ age_c + female + black + (black|state), data = polls, family = binomial(link = "logit")) arm::display(m2) ``` ``` ## glmer(formula = bush ~ age_c + female + black + (black | state), ## data = polls, family = binomial(link = "logit")) ## coef.est coef.se ## (Intercept) 0.43 0.07 ## age_c -0.08 0.02 ## female -0.11 0.04 ## black -1.66 0.19 ## ## Error terms: ## Groups Name Std.Dev. Corr ## state (Intercept) 0.44 ## black 0.87 -0.46 ## Residual 1.00 ## --- ## number of obs: 11566, groups: state, 49 ## AIC = 15100.6, DIC = 14697.4 ## deviance = 14892.0 ``` --- # Look at random effects ```r ranef_m2 <- tidy(m2, effects = "ran_vals", conf.int = TRUE) %>% arrange(level) ranef_m2 ``` ``` ## # A tibble: 98 x 8 ## effect group level term estimate std.error conf.low conf.high ## <chr> <chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl> ## 1 ran_vals state 1 (Intercept) 0.4768807 0.1716175 0.1405165 0.8132448 ## 2 ran_vals state 1 black 1.066314 0.4118905 0.2590240 1.873605 ## 3 ran_vals state 10 (Intercept) 0.3000900 0.08425460 0.1349540 0.4652259 ## 4 ran_vals state 10 black -0.1573061 0.3564817 -0.8559974 0.5413852 ## 5 ran_vals state 11 (Intercept) 0.2440973 0.1326607 -0.01591285 0.5041074 ## 6 ran_vals state 11 black -0.6672948 0.4129706 -1.476702 0.1421127 ## 7 ran_vals state 13 (Intercept) -0.2406066 0.2710096 -0.7717756 0.2905624 ## 8 ran_vals state 13 black 0.2180487 0.8103377 -1.370184 1.806281 ## 9 ran_vals state 14 (Intercept) -0.04190335 0.09568848 -0.2294493 0.1456426 ## 10 ran_vals state 14 black -0.3926602 0.3611247 -1.100452 0.3151311 ## # … with 88 more rows ``` --- # Include fixed effects ```r fe <- data.frame( fixed = fixef(m2), term = names(fixef(m2)) ) fe ``` ``` ## fixed term ## (Intercept) 0.43434106 (Intercept) ## age_c -0.08284379 age_c ## female -0.10836146 female ## black -1.66095113 black ``` ```r ranef_m2 <- left_join(ranef_m2, fe) ranef_m2 %>% select(level, term, estimate, fixed) ``` ``` ## # A tibble: 98 x 4 ## level term estimate fixed ## <chr> <chr> <dbl> <dbl> ## 1 1 (Intercept) 0.4768807 0.4343411 ## 2 1 black 1.066314 -1.660951 ## 3 10 (Intercept) 0.3000900 0.4343411 ## 4 10 black -0.1573061 -1.660951 ## 5 11 (Intercept) 0.2440973 0.4343411 ## 6 11 black -0.6672948 -1.660951 ## 7 13 (Intercept) -0.2406066 0.4343411 ## 8 13 black 0.2180487 -1.660951 ## 9 14 (Intercept) -0.04190335 0.4343411 ## 10 14 black -0.3926602 -1.660951 ## # … with 88 more rows ``` --- # Add in fixed effects ```r ranef_m2 <- ranef_m2 %>% mutate(estimate = estimate + fixed) ranef_m2 ``` ``` ## # A tibble: 98 x 9 ## effect group level term estimate std.error conf.low conf.high fixed ## <chr> <chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> ## 1 ran_vals state 1 (Intercept) 0.9112217 0.1716175 0.1405165 0.8132448 0.4343411 ## 2 ran_vals state 1 black -0.5946367 0.4118905 0.2590240 1.873605 -1.660951 ## 3 ran_vals state 10 (Intercept) 0.7344310 0.08425460 0.1349540 0.4652259 0.4343411 ## 4 ran_vals state 10 black -1.818257 0.3564817 -0.8559974 0.5413852 -1.660951 ## 5 ran_vals state 11 (Intercept) 0.6784383 0.1326607 -0.01591285 0.5041074 0.4343411 ## 6 ran_vals state 11 black -2.328246 0.4129706 -1.476702 0.1421127 -1.660951 ## 7 ran_vals state 13 (Intercept) 0.1937344 0.2710096 -0.7717756 0.2905624 0.4343411 ## 8 ran_vals state 13 black -1.442902 0.8103377 -1.370184 1.806281 -1.660951 ## 9 ran_vals state 14 (Intercept) 0.3924377 0.09568848 -0.2294493 0.1456426 0.4343411 ## 10 ran_vals state 14 black -2.053611 0.3611247 -1.100452 0.3151311 -1.660951 ## # … with 88 more rows ``` --- # Compute log-odds Compute means for each group - i.e., add the coefficients ```r to_plot <- ranef_m2 %>% group_by(level) %>% mutate(estimate = cumsum(estimate)) %>% ungroup() to_plot ``` ``` ## # A tibble: 98 x 9 ## effect group level term estimate std.error conf.low conf.high fixed ## <chr> <chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> ## 1 ran_vals state 1 (Intercept) 0.9112217 0.1716175 0.1405165 0.8132448 0.4343411 ## 2 ran_vals state 1 black 0.3165850 0.4118905 0.2590240 1.873605 -1.660951 ## 3 ran_vals state 10 (Intercept) 0.7344310 0.08425460 0.1349540 0.4652259 0.4343411 ## 4 ran_vals state 10 black -1.083826 0.3564817 -0.8559974 0.5413852 -1.660951 ## 5 ran_vals state 11 (Intercept) 0.6784383 0.1326607 -0.01591285 0.5041074 0.4343411 ## 6 ran_vals state 11 black -1.649808 0.4129706 -1.476702 0.1421127 -1.660951 ## 7 ran_vals state 13 (Intercept) 0.1937344 0.2710096 -0.7717756 0.2905624 0.4343411 ## 8 ran_vals state 13 black -1.249168 0.8103377 -1.370184 1.806281 -1.660951 ## 9 ran_vals state 14 (Intercept) 0.3924377 0.09568848 -0.2294493 0.1456426 0.4343411 ## 10 ran_vals state 14 black -1.661174 0.3611247 -1.100452 0.3151311 -1.660951 ## # … with 88 more rows ``` --- # Create factor level ```r lev_order <- to_plot %>% filter(term == "(Intercept)") %>% mutate(lev = forcats::fct_reorder(level, estimate)) to_plot <- to_plot %>% mutate(level = factor(level, levels = levels(lev_order$lev))) ``` --- # Plot ```r # data transform to_plot %>% mutate(group = ifelse(term == "(Intercept)", "Non-Black", "Black")) %>% # plot ggplot(aes(estimate, level)) + geom_line(aes(group = level), color = "gray60", size = 1.2) + geom_point(aes(color = group)) + geom_vline(xintercept = 0.5, color = "gray40", size = 3) + # themeing stuff labs(x = "Probability Estimate", y = "") + xlim(0, 1) + scale_color_brewer(palette = "Set2") + theme(panel.grid.major.y = element_blank(), axis.text.y = element_blank()) ``` --- # Plot <!-- --> --- # Probability scale ```r # data transform to_plot %>% mutate( group = ifelse(term == "(Intercept)", "Non-Black", "Black"), * prob = exp(estimate)/(1 + exp(estimate)) ) %>% # plot ggplot(aes(prob, level)) + geom_line(aes(group = level), color = "gray60", size = 1.2) + geom_point(aes(color = group)) + geom_vline(xintercept = 0.5, color = "gray40", size = 3) + # themeing stuff labs(x = "Probability Estimate", y = "") + xlim(0, 1) + scale_color_brewer(palette = "Set2") + theme(panel.grid.major.y = element_blank(), axis.text.y = element_blank()) ``` --- # Probability scale <!-- --> --- class: inverse-blue middle # Bayes --- # Refit Can you fit the same model we just fit, but with **{brms}**? You try first Feel free to just use flat priors <div class="countdown" id="timer_60b90b75" style="right:0;bottom:0;" data-warnwhen="0"> <code class="countdown-time"><span class="countdown-digits minutes">02</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">00</span></code> </div> --- # Flat priors ```r library(brms) m2_brms <- brm(bush ~ age + female + black + (black|state), data = polls, family = bernoulli(link = "logit"), backend = "cmdstan", cores = 4) ``` ``` ## Warning: Rows containing NAs were excluded from the model. ``` ``` ## - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - \ | / - Running MCMC with 4 parallel chains... ## ## Chain 1 Iteration: 1 / 2000 [ 0%] (Warmup) ## Chain 2 Iteration: 1 / 2000 [ 0%] (Warmup) ## Chain 3 Iteration: 1 / 2000 [ 0%] (Warmup) ## Chain 4 Iteration: 1 / 2000 [ 0%] (Warmup) ## Chain 2 Iteration: 100 / 2000 [ 5%] (Warmup) ## Chain 4 Iteration: 100 / 2000 [ 5%] (Warmup) ## Chain 1 Iteration: 100 / 2000 [ 5%] (Warmup) ## Chain 3 Iteration: 100 / 2000 [ 5%] (Warmup) ## Chain 2 Iteration: 200 / 2000 [ 10%] (Warmup) ## Chain 4 Iteration: 200 / 2000 [ 10%] (Warmup) ## Chain 1 Iteration: 200 / 2000 [ 10%] (Warmup) ## Chain 3 Iteration: 200 / 2000 [ 10%] (Warmup) ## Chain 2 Iteration: 300 / 2000 [ 15%] (Warmup) ## Chain 4 Iteration: 300 / 2000 [ 15%] (Warmup) ## Chain 1 Iteration: 300 / 2000 [ 15%] (Warmup) ## Chain 2 Iteration: 400 / 2000 [ 20%] (Warmup) ## Chain 3 Iteration: 300 / 2000 [ 15%] (Warmup) ## Chain 4 Iteration: 400 / 2000 [ 20%] (Warmup) ## Chain 1 Iteration: 400 / 2000 [ 20%] (Warmup) ## Chain 2 Iteration: 500 / 2000 [ 25%] (Warmup) ## Chain 3 Iteration: 400 / 2000 [ 20%] (Warmup) ## Chain 4 Iteration: 500 / 2000 [ 25%] (Warmup) ## Chain 2 Iteration: 600 / 2000 [ 30%] (Warmup) ## Chain 1 Iteration: 500 / 2000 [ 25%] (Warmup) ## Chain 3 Iteration: 500 / 2000 [ 25%] (Warmup) ## Chain 4 Iteration: 600 / 2000 [ 30%] (Warmup) ## Chain 2 Iteration: 700 / 2000 [ 35%] (Warmup) ## Chain 1 Iteration: 600 / 2000 [ 30%] (Warmup) ## Chain 3 Iteration: 600 / 2000 [ 30%] (Warmup) ## Chain 4 Iteration: 700 / 2000 [ 35%] (Warmup) ## Chain 2 Iteration: 800 / 2000 [ 40%] (Warmup) ## Chain 1 Iteration: 700 / 2000 [ 35%] (Warmup) ## Chain 3 Iteration: 700 / 2000 [ 35%] (Warmup) ## Chain 4 Iteration: 800 / 2000 [ 40%] (Warmup) ## Chain 2 Iteration: 900 / 2000 [ 45%] (Warmup) ## Chain 1 Iteration: 800 / 2000 [ 40%] (Warmup) ## Chain 3 Iteration: 800 / 2000 [ 40%] (Warmup) ## Chain 4 Iteration: 900 / 2000 [ 45%] (Warmup) ## Chain 2 Iteration: 1000 / 2000 [ 50%] (Warmup) ## Chain 2 Iteration: 1001 / 2000 [ 50%] (Sampling) ## Chain 1 Iteration: 900 / 2000 [ 45%] (Warmup) ## Chain 3 Iteration: 900 / 2000 [ 45%] (Warmup) ## Chain 4 Iteration: 1000 / 2000 [ 50%] (Warmup) ## Chain 4 Iteration: 1001 / 2000 [ 50%] (Sampling) ## Chain 2 Iteration: 1100 / 2000 [ 55%] (Sampling) ## Chain 1 Iteration: 1000 / 2000 [ 50%] (Warmup) ## Chain 1 Iteration: 1001 / 2000 [ 50%] (Sampling) ## Chain 4 Iteration: 1100 / 2000 [ 55%] (Sampling) ## Chain 3 Iteration: 1000 / 2000 [ 50%] (Warmup) ## Chain 3 Iteration: 1001 / 2000 [ 50%] (Sampling) ## Chain 2 Iteration: 1200 / 2000 [ 60%] (Sampling) ## Chain 1 Iteration: 1100 / 2000 [ 55%] (Sampling) ## Chain 4 Iteration: 1200 / 2000 [ 60%] (Sampling) ## Chain 2 Iteration: 1300 / 2000 [ 65%] (Sampling) ## Chain 3 Iteration: 1100 / 2000 [ 55%] (Sampling) ## Chain 1 Iteration: 1200 / 2000 [ 60%] (Sampling) ## Chain 4 Iteration: 1300 / 2000 [ 65%] (Sampling) ## Chain 2 Iteration: 1400 / 2000 [ 70%] (Sampling) ## Chain 1 Iteration: 1300 / 2000 [ 65%] (Sampling) ## Chain 3 Iteration: 1200 / 2000 [ 60%] (Sampling) ## Chain 4 Iteration: 1400 / 2000 [ 70%] (Sampling) ## Chain 2 Iteration: 1500 / 2000 [ 75%] (Sampling) ## Chain 1 Iteration: 1400 / 2000 [ 70%] (Sampling) ## Chain 4 Iteration: 1500 / 2000 [ 75%] (Sampling) ## Chain 2 Iteration: 1600 / 2000 [ 80%] (Sampling) ## Chain 3 Iteration: 1300 / 2000 [ 65%] (Sampling) ## Chain 1 Iteration: 1500 / 2000 [ 75%] (Sampling) ## Chain 4 Iteration: 1600 / 2000 [ 80%] (Sampling) ## Chain 2 Iteration: 1700 / 2000 [ 85%] (Sampling) ## Chain 1 Iteration: 1600 / 2000 [ 80%] (Sampling) ## Chain 3 Iteration: 1400 / 2000 [ 70%] (Sampling) ## Chain 4 Iteration: 1700 / 2000 [ 85%] (Sampling) ## Chain 2 Iteration: 1800 / 2000 [ 90%] (Sampling) ## Chain 1 Iteration: 1700 / 2000 [ 85%] (Sampling) ## Chain 4 Iteration: 1800 / 2000 [ 90%] (Sampling) ## Chain 3 Iteration: 1500 / 2000 [ 75%] (Sampling) ## Chain 2 Iteration: 1900 / 2000 [ 95%] (Sampling) ## Chain 1 Iteration: 1800 / 2000 [ 90%] (Sampling) ## Chain 4 Iteration: 1900 / 2000 [ 95%] (Sampling) ## Chain 2 Iteration: 2000 / 2000 [100%] (Sampling) ## Chain 2 finished in 41.0 seconds. ## Chain 1 Iteration: 1900 / 2000 [ 95%] (Sampling) ## Chain 3 Iteration: 1600 / 2000 [ 80%] (Sampling) ## Chain 4 Iteration: 2000 / 2000 [100%] (Sampling) ## Chain 4 finished in 41.9 seconds. ## Chain 1 Iteration: 2000 / 2000 [100%] (Sampling) ## Chain 1 finished in 42.7 seconds. ## Chain 3 Iteration: 1700 / 2000 [ 85%] (Sampling) ## Chain 3 Iteration: 1800 / 2000 [ 90%] (Sampling) ## Chain 3 Iteration: 1900 / 2000 [ 95%] (Sampling) ## Chain 3 Iteration: 2000 / 2000 [100%] (Sampling) ## Chain 3 finished in 48.2 seconds. ## ## All 4 chains finished successfully. ## Mean chain execution time: 43.5 seconds. ## Total execution time: 48.7 seconds. ``` --- # Model summary ```r summary(m2_brms) ``` ``` ## Family: bernoulli ## Links: mu = logit ## Formula: bush ~ age + female + black + (black | state) ## Data: polls (Number of observations: 11566) ## Samples: 4 chains, each with iter = 2000; warmup = 1000; thin = 1; ## total post-warmup samples = 4000 ## ## Group-Level Effects: ## ~state (Number of levels: 49) ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## sd(Intercept) 0.46 0.06 0.36 0.59 1.00 949 2013 ## sd(black) 0.96 0.20 0.61 1.41 1.01 1202 2403 ## cor(Intercept,black) -0.40 0.19 -0.71 0.02 1.00 1417 2354 ## ## Population-Level Effects: ## Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS ## Intercept 0.62 0.09 0.46 0.80 1.00 732 1254 ## age -0.08 0.02 -0.12 -0.05 1.00 5674 3257 ## female -0.11 0.04 -0.19 -0.03 1.00 5243 2793 ## black -1.67 0.22 -2.10 -1.24 1.00 1050 1688 ## ## Samples were drawn using sample(hmc). For each parameter, Bulk_ESS ## and Tail_ESS are effective sample size measures, and Rhat is the potential ## scale reduction factor on split chains (at convergence, Rhat = 1). ``` --- # Posterior predictive check ```r pp_check(m2_brms, type = "bars") ``` <!-- --> --- # Posterior predictive check 2 ```r pp_check(m2_brms, type = "stat") ``` <!-- --> --- class: inverse-green middle # Next time * More Bayes for binomial logistic regression * Plotting Bayes models * Missing data * Piece-wise growth models